| economy

This Bill Moyers interview with Simon Johnson is a must see. One of his main issues is that as long as we keep the bankers in power that caused this problem the problem will never be solved. Watch or read the interview.

Bill Moyers Journal with Simon Johnson

|

BILL MOYERS: Welcome to the Journal.

The battle is joined as they say — and here's the headline that framed it: "High Noon: Geithner v. The American Oligarchs." The headline is in one of the most informative new sites in the blogosphere called: baselinescenario.com. Here's the quote that grabbed me:

"There comes a time in every economic crisis, or more specifically, in every struggle to recover from a crisis, when someone steps up to the podium to promise the policies that — they say — will deliver you back to growth. The person has political support, a strong track record, and every incentive to enter the history books. But one nagging question remains. Can this person, your new economic strategist, really break with the vested elites that got you into this much trouble?"

And here's the man who asked that question. Simon Johnson is former chief economist at the International Monetary Fund. He now teaches global economics and management at MIT's Sloan School of Management and is a senior fellow of the Peterson Institute. He is co-founder of that website I quoted — baselinescenario.com — where he analyzes the global economic and financial crisis.

Welcome, Simon Johnson to the Journal.

SIMON JOHNSON: Nice to be here.

BILL MOYERS: What are you signaling with that headline, "Geithner vs. the American Oligarchs"?

SIMON JOHNSON: I think I'm signaling something a little bit shocking to Americans, and to myself, actually. Which is the situation we find ourselves in at this moment, this week, is very strongly reminiscent of the situations we've seen many times in other places.

But they're places we don't like to think of ourselves as being similar to. They're emerging markets. It's Russia or Indonesia or a Thailand type situation, or Korea. That's not comfortable. America is different. America is special. America is rich. And, yet, we've somehow find ourselves in the grip of the same sort of crisis and the same sort of oligarchs.

| |

[more]

Simon Johnson's website is a must read.

The Baseline Scenario

Every Consensus Must End

|

The prevailing consensus on any economic policy is a fascinating beast. For years it can stay put, seemingly immovable, and even - in some cases - becoming enshrined in legislation or central bank statute. One day it begins to shake, ever so slightly; under the pressure of events, a wider range of serious opinion develops. And then, all of a sudden, the consensus breaks and you are running hard to keep up.

We saw this last year with regard to discretionary fiscal policy - fiscal stimulus - in the US. Eighteen months ago, very few mainstream economists or other policy analysts would have suggested that the US respond to the threat of recession with a large spending increase/tax cut. The consensus - based on long years of experience and research - was that discretionary fiscal policy generates as many problems as it solves. To argue against this consensus was to bang your head against a brick wall, while also being regarded as not completely serious.

At some point in November/December 2007, this consensus began to shake. The history may prove controversial but my perspective at the time and in retrospect is that Marty Feldstein was the first heavyweight economist to question the consensus (including in interactions on Capitol Hill), and he was followed closely by Larry Summers’ influential writings in the Financial Times. Within a month or so, the consensus broke. Not only did we get a fiscal stimulus in early 2008 for the US, but the IMF quickly adopted the same pro-stimulus line globally and the terms of the debate changed everywhere. This fed into a process out of which came at least a temporary new quasi-consensus: a large US fiscal stimulus is part of the sensible policy mix today.

The consensus on banking just broke cover. For some weeks it has been under intense pressure. At least since the fall, serious people have been informally floating various new ideas on how to deal with the technical problems surrounding toxic assets and presumed deficient bank capital. But since mid-January, the mainstream consensus - that we should protect existing large banks and keep them in business essentially “as is” - seems to have cracked.

Paul Romer and Willem Buiter favor an approach that emphasizes the creation of new banks. Roger Farmer wants to go in a completely different direction. These are just a few examples of the great (and completely constructive) new dispersion of ideas around banking - post links to your favorite new ideas in comments below.

| |

[more]

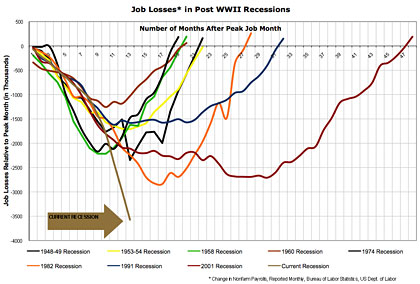

How Bad Is It? Job Losses in Post WWII Recessions

[more]

Meltdown Madness

The Human Costs of the Economic Crisis

|

The body count is still rising. For months on end, marked by bankruptcies, foreclosures, evictions, and layoffs, the economic meltdown has taken a heavy toll on Americans. In response, a range of extreme acts including suicide, self-inflicted injury, murder, and arson have hit the local news. By October 2008, an analysis of press reports nationwide indicated that an epidemic of tragedies spurred by the financial crisis had already spread from Pasadena, California, to Taunton, Massachusetts, from Roseville, Minnesota, to Ocala, Florida.

In the three months since, the pain has been migrating upwards. A growing number of the world's rich have garnered headlines for high profile, financially-motivated suicides. Take the New Zealand-born "millionaire financier" who leapt in front of an express train in Great Britain or the "German tycoon" who did much the same in his homeland. These have, with increasing regularity, hit front pages around the world. An example would be New York-based money manager René-Thierry Magnon de la Villehuchet, who slashed his wrists after he "lost more than $1 billion of client money, including much, if not all, of his own family's fortune." In the end, he was yet another victim of financial swindler Bernard Madoff's $50 billion Ponzi scheme.

An unknown but rising number of less wealthy but distinctly well-off workers in the financial field have also killed themselves as a result of the economic crisis -- with less press coverage. Take, for instance, a 51-year-old former analyst at Bear Stearns. Learning that he would be laid off after JPMorgan Chase took over his failed employer, he "threw himself out of the window" of his 29th-floor apartment in Fort Lee, New Jersey. Or consider the 52-year-old commercial real estate broker from suburban Chicago who "took his life in a wildlife preserve" just "a month after he publicly worried over a challenging market," or the 50-year-old "managing partner at Leeward Investments" from San Carlos, California, who got wiped out "in the markets" and "suffocated himself to death."

| |

[more]

On The Edge

By Paul Krugman

|

Would the Obama economic plan, if enacted, ensure that America won't have its own lost decade? Not necessarily: a number of economists, myself included, think the plan falls short and should be substantially bigger. But the Obama plan would certainly improve our odds. And that's why the efforts of Republicans to make the plan smaller and less effective - to turn it into little more than another round of Bush-style tax cuts - are so destructive.

So what should Mr. Obama do? Count me among those who think that the president made a big mistake in his initial approach, that his attempts to transcend partisanship ended up empowering politicians who take their marching orders from Rush Limbaugh. What matters now, however, is what he does next.

It's time for Mr. Obama to go on the offensive. Above all, he must not shy away from pointing out that those who stand in the way of his plan, in the name of a discredited economic philosophy, are putting the nation's future at risk. The American economy is on the edge of catastrophe, and much of the Republican Party is trying to push it over that edge.

| |

[more]

Asia: The Coming Fury

As goods pile up in wharves from Bangkok to Shanghai, and workers are laid off in record numbers, people in East Asia are beginning to realize they aren't only experiencing an economic downturn but living through the end of an era.

|

For over 40 years now, the cutting edge of the region's economy has been export-oriented industrialization (EOI). Taiwan and Korea first adopted this strategy of growth in the mid-1960s, with Korean dictator Park Chung-Hee coaxing his country's entrepreneurs to export by, among other measures, cutting off electricity to their factories if they refused to comply.

The success of Korea and Taiwan convinced the World Bank that EOI was the wave of the future. In the mid-1970s, then-Bank President Robert McNamara enshrined it as doctrine, preaching that "special efforts must be made in many countries to turn their manufacturing enterprises away from the relatively small markets associated with import substitution toward the much larger opportunities flowing from export promotion."

EOI became one of the key points of consensus between the Bank and Southeast Asia's governments. Both realized import substitution industrialization could only continue if domestic purchasing power were increased via significant redistribution of income and wealth, and this was simply out of the question for the region's elites. Export markets, especially the relatively open U.S. market, appeared to be a painless substitute.

| |

[more]

No Banks Means No Banking Crisis

by Ian Welsh

|

Stiglitz is saying something slightly more radical than what I've been saying for some time. You don't need the current banks. If they won't lend, let them go under. If the Fed can lend to banks, why can't it lend directly to banks and consumers.

Banks exist to be intermediaries between central banks and those who need credit. They are given the ability to create money through fractional reserve money (yes, create) and they also have the right to borrow money at rates that no one else can receive. If you could take your money, multiply it by 10 (that's not the exact number, but as an example) and lend it out, think you could make a profit? If you could borrow money at 1 to 5% and then lend it out for more than that, in some cases 15% more, think you could make money?

Banks thus are given by governments an incredibly valuable privilege. It's really hard to overstate how easy it is to make steady returns as a bank as long as you don't get greedy. In exchange for the right to create money and borrow it at rates no one else gets, banks are expected to add some value to the equation. Specifically, they are expected to figure out who is a good credit risk, and where money should best be loaned and used. There are two sides of this - money should be loaned where it has a high return. It should also be loaned to folks who can pay it back. It should be invested in the same way—return averaged with risk.

Banks haven't been doing this.

| |

[more]

The Choice: A Generation of A Lousy Economy, Or?

by Ian Welsh

|

Yesterday I discussed the "let the banks go under" option. Let's talk about the ups and downs of this possibility, because there are significant risks associated with it, which is why folks like Summers and Geithner are acting like they stared at the Gorgon and have been turned to stone.

The case for it is simple enough: if you don't force the losses and the write downs, and instead allow a combination of impaired bank balance books and government accepting the losses, whether through a bad bank, insurance or other means, you have to write off trillions and trillions (I'm guessing, globally, a minimum of 8 trillion, and it is probably much higher than that). That money will not be available for useful investments, for income, for social security or anything else. It will be commited for a generation. This is essentially what happened in Japan, when Japan refused to have its banks really accept and acknowledge their losses. If you're old enough, you remember the days when Japan had probably the world's most dynamic economy. No longer, instead they have an economy that's in and out of the hospital, one where the good times have never, ever returnred.

That's the zombie bank route combined with a bad bank that doesn't nationalize banks. Pay it off over a generation.

This method has the advantage (from the point of view of decision makers) that it leaves the same class of people in charge of the economy. From the point of view of ordinary citizens that's probably a bad thing, since the current elites are not only incompetent, they are wedded to old infrastructure and and old model of organizing the economy. Just as England did not succesfully make the leap from a coal economy to an oil economy in time to avoid its own fall, current interests are stoppng America from investing in the future—whether that is true in the internet, where the US has awful broadband compared to its competitors or in new energy technology, where others are ahead in solar wind and indeed virtually every renewable technology. Keep these folks in charge, and this will continue.

Now the problem with letting banks go under instead is that it forces an acknowledgment of losses in a short period.

| |

[more] |